I’ve talked a lot about how much it takes to retire and safe withdrawal rates and ways to increase safe withdrawal rates. See the series of posts here. All of these discussions and studies I reference are based on a certain retirement model. Lets call it the portfolio value retirement model. One critical assumption in that model is that it assumes re-investment of all stock dividends and income from bonds and relies on selling off assets yearly to fund retirement spending needs. This assumption makes the longevity of a retirement portfolio critically dependent on big down years in the value of the portfolio. I think there is a better and simpler retirement model – the dividend retirement model.

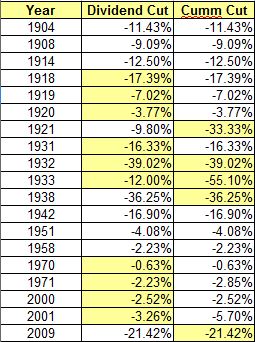

A dividend retirement model is one where an investor lives off the dividend income received from their retirement portfolio. No asset sales are required to fund retirement. So, if you have a portfolio that yields 4%, you live off that 4%. Simple. In such a model, the market prices of the stocks, the value of the portfolio, are much less important than in the other model. However, other factors are much more critical. In the dividend retirement model, the stability/consistency of the dividend stream and its growth relative to inflation are the most critical parameters. Lets look at the history of both these factors to see how feasible such a retirement model is. We’ll use the S&P500 index, the same index used in the traditional retirement model. Using the dividend history of the index going back to 1900, the inflation adjusted (real) growth in dividends has been 1.2%. Thus, dividend growth from the index has been enough keep up with inflation. The second test is more difficult – the stability of the dividends. The table below shows every year since 1900 where there was a reduction in the S&P500 dividends and the extent of the reduction.

{kind=link}

The first column shows the dividend reduction in a given year and the second column shows the cumulative reduction in the cases there were several years in a row of cuts. The first column highlights those years with sequential reductions and the second column highlights cumulative reductions above 20%. Not very stable and some very large reduction in dividends that would make living off the S&P500 dividend stream near impossible. And this is the reason I think most academics, financial planners, don’t even discuss the dividend retirement model. Based on the S&P500, it is not a feasible model. Since most academics, financial planners, are efficient market proponents anyway, the conclusion is that an investor cannot do better than this. Well, BS.

In order to implement the dividend retirement model, an investor cannot rely on indexes due to the instability of the dividend stream. The investor needs to invest in a portfolio of dividend paying stocks with consistent and rising dividends. This is not as difficult as it sounds. There are many stocks that have long histories of steady and rising dividends. A good reference on these dividend stocks lists can be found here. For example, the S&P dividend aristocrats are a group of 42 companies in the S&P500 that have raised dividends for at least 25 years in a row. And if you remove the large cap requirement, the US dividend champions list, also with 25 consecutive years of payments and growth, has over 200 members. In addition, there even are larger lists of 10 year payers, up and coming payers etc… And many of these lists do not even include stocks such as REITs, MLPs, and international stocks which can enhance yields further. I’ll post more on these lists in the future and some more thoughts on portfolio construction but the point is there is a large pool of consistent quality dividend payers to fund a stable retirement.

Outside of choosing consistent dividend payers with long track records, at least 10 years I would say, a dividend retiree can add an additional layer of safety by having a dividend income buffer. For example, I personally use an income buffer of 20%. If my retirement income needs are $40K then I target a dividend income from my portfolio of $50K. This way I can target a worst case dividend cut of 20% across my portfolio, a very dire assumption if one is choosing the right dividend stocks. Such a strategy allows me to sleep much easier at night knowing that one unforeseen dividend cut will not impact my income requirement for the year.

Another upshot of the dividend retirement model is the lesser importance of the value of the portfolio as determined by the price of the stocks in the portfolio or the price of the market indexes for that matter. As long as the dividend is stable and growing more than inflation, the value of the portfolio, prices of stocks, is of much less importance to retiree. We know that in the long run dividends and dividend growth account for most of stock’s returns but there can be long periods of mispricings and under performance. This is yet another layer of comfort with such a portfolio. I like to use JNJ as an example here. Over the last 10 years JNJ’s stock price has basically been flat but during that same time it’s dividend growth rate has been 13% per year. If I’m using JNJ’s dividend as a piece of my retirement income stream I feel pretty darn good despite the flat stock price.

In summary, I think its quite realistic and feasible to build a safe portfolio of dividend paying stocks that funds an investor’s retirement needs adjusted for inflation. Most planners seem to dismiss such a model due to the poor history of the S&P500 with respect to the stability of dividends and the fact that most advisors/planners don’t believe in active investing anyway. This is very unfortunate because such a model can provide a safe, comfortable, and peaceful retirement. I’ll continue to post on the portfolio value retirement model because that is what the majority of retirees will still use and there are ways to improve that model but the dividend retirement model is my preferred method of funding my retirement.

12 Comments

J Carroll · March 4, 2011 at 4:57 pm

Paul, very good and helpful article; hits my nail right on the head and I have been evolving toward the MLPs, REITs, div paying domestic stocks, and international div paying stocks for several years now. The area most difficult to utilize is international div paying stocks; so many of the non-US companies distribute only twice, or even only once, per year. I use ETFs to access this area; currently DWX, and I hope Vanguard will soon open an ETF that invests in this area. Will you offer ideas on how to best access international div paying stocks, in a way that provides income at least quarterly? Thank you.

libertatemamo · March 5, 2011 at 9:18 am

Sure J. I’ll look into source for int’l div stocks. Not many pay div quarterly. I have no issues with twice a year or even annual div payments so that opens up the landscape of opportunities quite a bit. Two of my favorite int’l holdings right now are FFH.TO (FRFHF.PK) and NGG.

Paul

Doug · March 5, 2011 at 7:36 am

Great Paul. I have begun in this direction this year with plans similar to J Carroll and will also focus a percentage of the stock and fixed income allocations to CEFs where dividends are good.

Keep the articles coming…I really look forward to them!

libertatemamo · March 5, 2011 at 9:15 am

Thanks Doug.

Dotcom · March 5, 2011 at 12:48 pm

I am extremely interested in this topic and currently have 20% of my portfolio allocated to dividend producing stocks, bonds, Bond Funds, CDs, ETFs, MLPs and Preferred’s. Outside of these dividend paying products I also own some mutual funds.

I have been reading Seeking Alpha articles about dividend investing for a couple of years now and that has resulted in my adding approximately 12 dividend paying stocks.

I recently read an article by Dave Van Knapp (last week) that entertains the same notion that your article addresses, i.e. building a dividend portfolio with dividend aristocrats, achievers, champions and MLPs to achieve a safe, decent and growing yield to live off of during retirement, keep up with inflation…

One key question is what percentage of a portfolio do you allocate to dividend paying stocks & MLPs? Since this thinking seems somewhat new or it’s at least new to me. I get a little anxious when considering, for example, putting 100% of a 1 million dollar portfolio into dividend aristocrats, champions & achievers. Maybe I shouldn’t be, but I need to better understand the potential risks and rewards. I also need to understand how to balance out such a portfolio, e.g. add TIPS, bonds, bond funds, CDs… Maybe I’m answering my own questions as I write this, so my main question remains what is a smart, safe, healthy portfolio percentage to allocate to this strategy?

I plan on sneaking up to 25%, then 30%… and seeing how it goes, hoping that my dividend income reaches a point of providing my full living expenses + a buffer similar to what you indicate (20%).

libertatemamo · March 6, 2011 at 10:06 am

Dotcom, congrats on getting started on the dividend path. Van Knapp writes some good articles as well as some others on Seeking Alpha. You raise some great portfolio allocation questions. Here are my thoughts.

Portfolio allocation is highly individual and I think highly driven by personal tolerances of volatility. Lets say you can build a div stock portfolio with 100% of your liquid assets that generates all the income you need plus buffer. Could you tolerate a 50% drop in the value of the portfolio even if no dividend is cut? The logical, rational answer is yes, of course, my income from dividends remains intact. In reality, most investors cannot tolerate such a drop emotionally and end up selling at the absolute worst times. So, even though that 100% div stock portfolio may be the best one that generates the most long term wealth it is not realistic for most investors.

Personally, I keep anywhere between 20-40% of my portfolio in non-stock assets. Currently, I’m about 30%. I rarely find opportunities to be 100% invested in div stocks. May 2009 was the last time I was buying hand over fist and went down to less than 10% cash. I use my non-stock assets to trade more aggressive income strategies like options. This model works for me.

So, I think every income investor needs to find a personal balance between generating enough income for retirement, having enough stock assets to build long term wealth, and meet their individual risk tolerances. I’ll be posting more on asset allocation in retirement but hopefully these considerations get you thinking in the right direction.

Paul

Jr. Executive · August 31, 2012 at 4:37 pm

New to the site and I’m catching up on historical posts. I’m clearly an advocate of the dividend retirement model, having initiated a methodical entry to my primary portfolio starting in early 2009 and taken the critical “plunge” of early retirement in 2011.My wife and I use a 4-tier approach to our finances (tier 1 – short term expenditure needs for next 5 years, tier 2 – expenditure needs for years 6-14, tier 3 – expenditure needs for years 15-24, and tier 4 – expenditure needs for years 25+). Each tier has a varying dividend yield target allowing for mix of growth and immediate yield. Since there is a 10 year age gap between us, it’s important to have a tier that isn’t expected “to be tapped” until mandated by current tax law at age 70.5 for my wife, hence the 25+ year tier. I’ll pull together some of the information sources we utilize in filtering candidates as well as some of the parameters that are utilized in making an investment decision.

I’ve enjoyed looking over the posts so far. I hope you have continued success.

libertatemamo · August 31, 2012 at 8:52 pm

Glad you’re enjoying the blog.

Paul

Death by bonds « Investing For A Living · March 6, 2011 at 1:27 pm

[…] you look at the research on safe withdrawal rates (my posts on it here) in retirement, using the portfolio value retirement model, you find that replacing the bond component of retirement portfolios with money market funds makes […]

The investing for a living retirement model « Investing For A Living · March 29, 2011 at 12:36 pm

[…] model is in the way dividends are used. As opposed to simply living off the dividends, as I discuss here, ideally I would like the enhanced return that comes from the reinvestment of dividends. However, I […]

The importance of valuation for income investors « Investing For A Living · April 8, 2011 at 4:17 pm

[…] dividends. This could be an investor building wealth towards retirement or a retiree following the standard retirement model where an investor reinvests dividends and sells off assets to fund retirement. This investor was […]

Investing for a living top 10 posts on dividends « Investing For A Living · February 4, 2012 at 12:32 pm

[…] Dividends – a better retirement model – a retirement model based on dividend income is superior to other retirement models […]

Comments are closed.